Projections show a 6–8% compound annual growth rate (CAGR) for microsilica between 2026 and 2030, yet this expansion hides a far more critical story: supply chain compression at the high-purity end. Engineers specifying 94% SiO₂ or higher for ultra-high-performance concrete (UHPC) and advanced refractories will face tightening lead times and steeper cost curves if they do not align procurement strategies with the shifting global production map.

Macro-Driven Demand: Where the Next 1.2 Million Tonnes Will Be Consumed

Asia-Pacific already accounts for 62% of global microsilica consumption, and that share is rising. China’s Belt and Road infrastructure portfolio alone is estimated to require an additional 180,000 tonnes annually by 2028, driven by high-speed rail, sea‑crossing bridges, and deep‑water port projects where UHPC’s 150 MPa+ compressive strength and chloride resistance are non-negotiable. India’s National Infrastructure Pipeline, with USD 1.4 trillion in sanctioned spend, mandates high‑performance concrete (HPC) in all national highway and metro rail expansions, pushing its annual silica fume imports past the 70,000-tonne mark by 2027.

Meanwhile, the Middle East is accelerating beyond high‑rise into giga‑projects. NEOM’s linear city alone specifies microsilica in 80% of its cast‑in‑place concrete elements to meet a 100‑year service‑life requirement in extremely aggressive sulfate soils. Across the Atlantic, North America’s IIJA‑funded bridge rehabilitation programme will consume an estimated 45,000 tonnes of silica fume per year from 2026 onward — predominantly 92% and 96% SiO₂ densified grades — as state DOTs rewrite specifications to eliminate high‑permeability concrete from freeze‑thaw zones.

UHPC: The Concentration of Value in a 4% Volume Sector

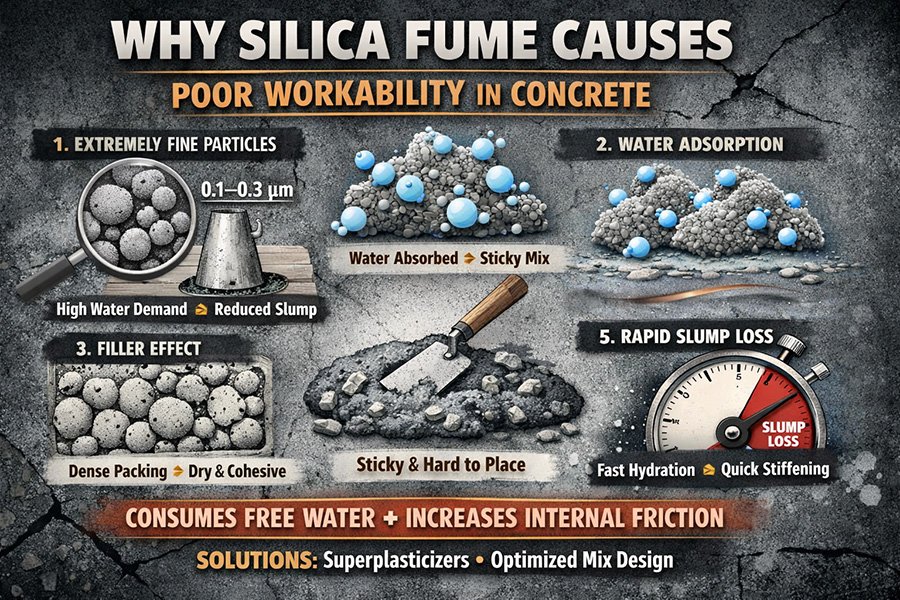

Ultra‑high‑performance concrete consumes less than 4% of total silica fume volume globally, yet it exerts disproportionate influence on the market’s value chain. A typical UHPC mix demands 250–350 kg of microsilica per cubic metre (bwoc basis), up to three times the dosage in conventional HPC. With UHPC production forecast to exceed 1.5 million cubic metres annually by 2030, the grade‑specific pull on 96% and 98% SiO₂ microsilica is unlike anything seen in ordinary concrete sectors. European precasters now routinely specify BET surface areas above 20 m²/g and loss on ignition (LOI) below 1.5% to ensure consistent rheology with PCE superplasticizers, a requirement that filters out low‑reactivity material sources.

This tight specification band concentrates demand on a limited number of furnaces capable of yielding such purity. As a result, price premiums for 98% SiO₂ densified silica fume have widened to 18–22% above mid‑grade material, a gap that is forecast to persist through 2030 as field performance data from the 2017‑built UHPC bridges in South Korea and Malaysia continues validating the material‑cost‑to‑lifecycle‑benefit ratio. Engineers designing with K-UHPC or AFGC recommendations will find that accepted silica fume sources become the critical path item for project budgets, not cement or steel fibre.

Refractory Castables: How the Iron‑ and Steel‑Making Cycle Reshapes Off‑Take

Refractory applications represent the second‑largest end‑use, heavily geared to crude steel output. Global steel production is projected to grow at 1.8% annually to 2.2 billion tonnes by 2030, with electric‑arc furnace (EAF) share rising from 29% to 35%. EAF roofs and delta sections demand low‑cement castables with 6–8% undensified silica fume addition to achieve the hot modulus of rupture above 18 MPa at 1400°C. This shift favors undensified grades with bulk density below 350 kg/m³, because densified forms can introduce particle packing inconsistencies during dry‑mix blending in automated refractory batching towers.

Suppliers serving the refractory sector are already seeing changes in order patterns. Quarterly demand for undensified silica fume used for refractory applications has become more volatile, tracking iron‑ore price cycles with a lag of approximately four months. Buyers hedging against spot‑price spikes are increasingly moving to semi‑annual contracts with fixed SiO₂ windows, a trend that will likely standardize 92% and 94% grades as the refractory industry’s default specification by 2028. Meanwhile, the rise of green steel — hydrogen‑based direct‑reduced iron — may shift refractory demand toward higher‑alumina systems, but silica fume will remain the silica carrier of choice in mainstream castables through 2030.

Grade Fragmentation and Why 85% Material Is Gaining New Relevance

Not all growth is at the purity ceiling. A parallel trend is the re‑legitimization of 85% SiO₂ silica fume for non‑structural applications, driven by carbon‑credit quantification. Soil stabilization programmes in the Gulf Cooperation Council (GCC) countries are now specifying silica fume as a partial cement replacement in deep‑soil mixing, where the pozzolanic reaction threshold can be met with 85% material at a delivered cost 22–25% lower than 92% grades. A 2025 trial by Abu Dhabi’s Department of Municipalities and Transport demonstrated that a 10% silica fume addition reduced the permeability of sabkha‑treated soil by two orders of magnitude, making 85 silica fume for cement‑based grouting a commercially viable specification for the region’s USD 3.8‑billion flood mitigation programme.

This grade fragmentation is reshaping logistics. Distributors that once stocked only 92% material now carry three SiO₂ tiers and both densified and undensified formats, increasing warehousing complexity but capturing margins from smaller‑volume, high‑frequency buyers. For buyers, the key risk is contamination: an 85% grade intermixed with a 92% delivery can alter w/b ratio and slump retention enough to fail a UHPC pre‑qualification trial. Chain‑of‑custody documentation, including furnace‑lot traceability, will become a procurement non‑negotiable by 2027.

Regional Supply Shifts: China’s Capacity Consolidation and Its Ripple Effects

China produces approximately 70% of the world’s microsilica, yet environmental enforcement is closing 15–20% of older ferrosilicon and silicon‑metal furnaces that lack waste‑heat recovery systems. This capacity rationalization will net out a modest global supply reduction of 3–5% by 2028, but the real impact is grade‑specific. Furnaces that produced borderline 92% material are being retired, while newer operations with fume baghouse upgrades consistently yield 96–98% SiO₂. The resulting shift in the supply mix means that mid‑grade availability tightens faster than high‑grade, an inversion of the typical premium‑product scarcity curve.

Below is a comparison of regional demand growth by application, reflecting the compound shifts described above.

| Region | Primary Demand Driver | 2025-2030 CAGR | Key Grade |

|---|---|---|---|

| Asia‑Pacific | UHPC bridges, high‑rise | 7.8% | 92%–96% densified |

| Middle East & Africa | Marine infrastructure, soil stabilization | 9.1% | 85%–92% densified |

| Europe | Precast UHPC, repair mortars | 5.4% | 96%–98% densified |

| North America | Bridge deck overlays, precast | 5.9% | 92% densified |

| Latin America | Mining shotcrete, refractory | 6.2% | 92% undensified |

The supply concentration risk is prompting bulk buyers to evaluate multi‑source frameworks. Specifications such as EN 13263‑1 permit blending of approved sources, a philosophy that will become operationalised as project owners pressure EPC contractors to qualify at least two silica fume suppliers per concrete mix design. For procurement teams, the winning formula is a long‑term alliance with a supplier whose own raw‑material consolidation — across multiple furnace operations — guarantees grade consistency without reliance on a single furnace line.

Technology Substitution Threats and Why They Won’t Materialize Before 2032

Metakaolin, rice‑husk ash, and synthetic nanosilica are often positioned as silica fume replacements, but a techno‑economic evaluation shows they will not displace microsilica at scale within this forecast window. Metakaolin’s specific surface area of 15–20 m²/g yields excellent pozzolanic reactivity, but its platelet morphology increases water demand by 12–15% compared to spherical silica fume in equivalent dosage, limiting its use in self‑consolidating UHPC where the w/b ratio stays below 0.20. Rice‑husk ash can reach 90%+ SiO₂ but suffers from uncontrolled carbon content (LOI up to 10%) that interferes with air‑entraining admixtures, a disqualifier for freeze‑thaw‑exposed HPC. Nanosilica, even at 5–10 nm particle size, costs 8–12 times more per kilogram of reactive silica and exhibits agglomeration challenges that currently restrict its use to premium repair mortars.

Instead, the near‑term innovation is not substitution but synergistic combination. Several of the microsilica concrete advantages — particle packing at the ITZ, accelerated C‑S‑H gel formation, and bleeding suppression — are amplified when a small fraction (2–3% bwoc) of nanosilica is blended with microsilica. This hybrid approach is already appearing in proprietary bridge‑deck overlay systems in Scandinavia, pointing to a 2027–2029 adoption curve rather than outright replacement.

Other sectors undergoing re‑evaluation include oil‑well cementing, where micro silica fume for refractory‑style performance is required at bottom‑hole static temperatures above 150°C. Silica fume additions of 35–40% bwoc prevent strength retrogression in geothermal and deep HPHT wells, a segment projected to grow at 4.2% annually as national oil companies in Southeast Asia and East Africa sanction deeper offshore development wells. Here, the silica fume must be low in calcium and alkali to avoid early‑age gelation with high‑temperature retarders — a further specification layer that consolidates business around suppliers with dedicated furnace runs and segregated storage.

Finally, silica fume for soil stabilization is expanding beyond arid‑zone sabkha treatment into soft‑clay stabilization for Southeast Asian logistics hubs. Thailand’s Eastern Economic Corridor has trialled 8% silica fume‑by‑dry‑soil in container yard subgrades, recording CBR improvements from 2.5% to 18% after 28 days of ambient curing. This application, while consuming mainly 85–92% grades, adds a new demand vector that most market models overlooked two years ago. By 2030, soil stabilization could absorb 5% of global silica fume output, underscoring the point that forecasting the microsilica market requires looking far beyond concrete cylinders.

Frequently Asked Questions

Q: What is the expected global CAGR for the microsilica market from 2026 to 2030?

A: Based on infrastructure spending pipelines and UHPC adoption rates, the global microsilica market is forecast to grow at a CAGR of 6-8% through 2030, with the Asia-Pacific and Middle East regions exceeding 7.5% annually.

Q: Which silica fume grade will see the fastest demand growth?

A: 96% and 98% SiO₂ grades will experience the fastest proportional growth due to UHPC and high-performance refractory specifications, but 85% grade is gaining new volume in soil stabilization projects where cost-per-tonne of reactive silica is the primary driver.

Q: Will silica fume supply keep up with demand through 2030?

A: Total global supply will remain adequate, but mid-grade (92% SiO₂) availability will tighten disproportionately as older Chinese furnaces are retired. Procurement teams should qualify at least two grade-consistent sources per concrete mix design to mitigate regional shortfalls.

Q: Are alternative pozzolans likely to replace microsilica in concrete before 2030?

A: No. Metakaolin, rice-husk ash, and nanosilica serve niche roles but cannot match silica fume’s combination of spherical particle morphology, low LOI, and proven field performance at competitive cost within this forecast window. Near-term innovation lies in hybrid blends, not outright replacement.

Q: What specification standard is most commonly referenced for microsilica in infrastructure projects?

A: ASTM C1240 (Standard Specification for Silica Fume Used in Cementitious Mixtures) in the Americas and Asia-Pacific, and EN 13263 in Europe, both govern chemical and physical requirements. Projects often layer additional limits on LOI (<1.5%), SiO₂ (>92%), and +45 µm sieve retention (<1.5%) for UHPC applications.

About Henan Superior Abrasives (HSA)

Henan Superior Abrasives (HSA) is a China-based global supplier of high-quality silica fume (microsilica) for concrete and refractory applications. Supplying both densified and undensified grades compliant with ASTM C1240 and EN 13263, HSA serves customers in 30+ countries with reliable microsilica solutions for HPC, UHPC, precast concrete, shotcrete, and other high-performance construction materials.

Get a Quote or Free Sample

Ready to improve your concrete performance with premium silica fume? Contact our technical team today — we respond within 24 hours and can arrange free samples for qualified projects.

- 📧 Email: sales@superior-abrasives.com

- 💬 WhatsApp: +86-186-3863-8803